Roof to Wall Straps Wind Mitigation: Straps vs Clips vs Toenails (and How Inspectors Prove It)

This guide focuses on roof to wall straps wind mitigation and the exact photo proof inspectors use so your credits don’t get downgraded. Roof to wall straps wind mitigation credits can meaningfully reduce the wind portion of a Florida homeowners premium—but this category is also one of the easiest to

Opening Protection Wind Mitigation: 9 Critical Proof Steps to Avoid Costly Credit Loss (Weakest-Opening Rule)

Opening Protection Wind Mitigation: The Weakest-Opening Rule (and How to Document It So Credits Don’t Disappear) Opening protection wind mitigation credits can lower the wind portion of your homeowners insurance—until underwriting reviews the file and downgrades it. The reason is brutally simple: opening protection is not “most openings.” It’s every

Secondary Water Resistance Florida: 7 Critical Proof Steps to Get the SWR Credit (and Avoid Costly Downgrades)

Secondary water resistance Florida is one of the most misunderstood wind-mitigation credits. Homeowners think “I have underlayment, so I qualify.” Underwriting thinks “prove it.” And if you can’t prove it, the credit gets downgraded. On Florida’s wind mitigation form (OIR-B1-1802), the SWR section is blunt: standard underlayments or hot-mopped felts

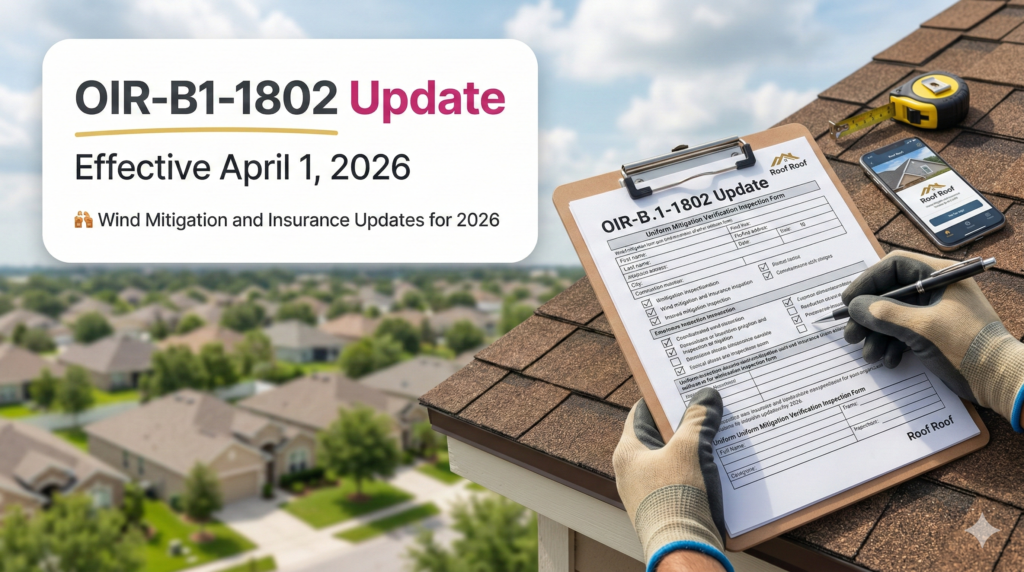

OIR-B1-1802 Form April 1 2026: 9 Critical Changes Homeowners Must Know to Avoid Costly Wind Credit Downgrades

The OIR-B1-1802 form April 1 2026 update is official—and it matters for wind mitigation credits.. The biggest mistake homeowners make is assuming “I have upgrades, so I’ll get credits.” In reality, credits are awarded for verified features + insurer-acceptable proof. If the proof is weak, the credits get downgraded—even if

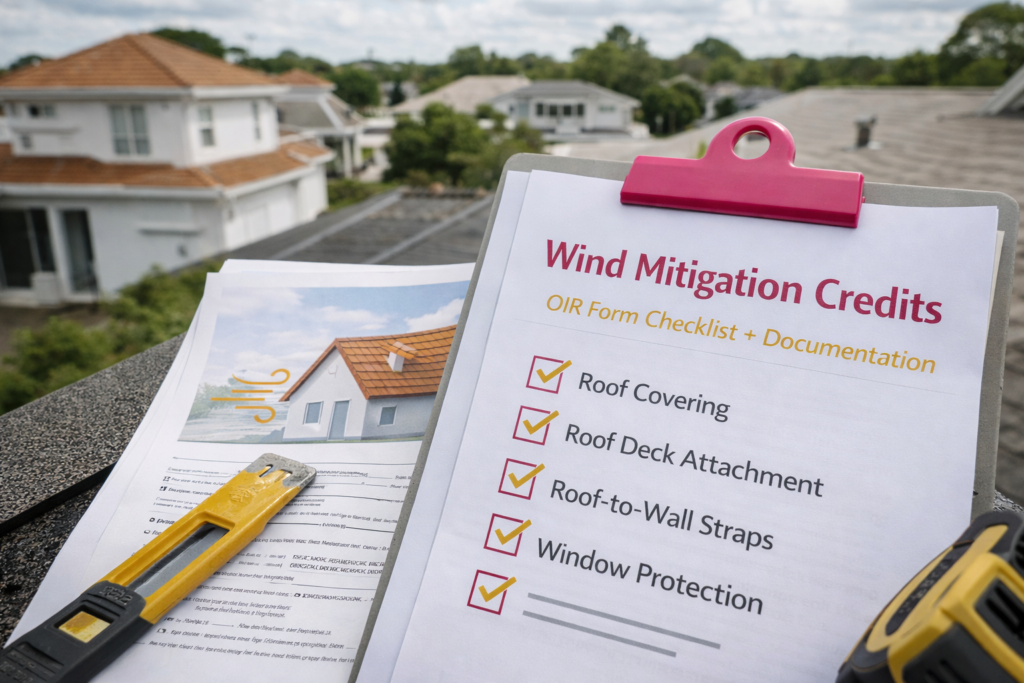

🌬️Wind Mitigation Credits: 9 Things Inspectors Look for on the OIR Form—and How to Document It to Lower Premiums

Wind mitigation credits can reduce the windstorm portion of your homeowners insurance premium—but only if your home’s features are verified and documented the way insurers expect. In Florida, that verification is done on the state’s Uniform Mitigation Verification Inspection Form (OIR-B1-1802). Here’s the truth: most “lost discounts” don’t happen because